Property developers should pay careful attention to the treatment of GST in contracts for the sale of land. Recently, two developers in dispute incurred significant costs and delays simply over missing the word “Plus” in a contract of sale.

Many experienced property developers would be familiar with the standard form contract of sale of real estate in Victoria. It provides that the price includes GST (if any) unless the particulars of sale specifically state that the price is “Plus GST”.

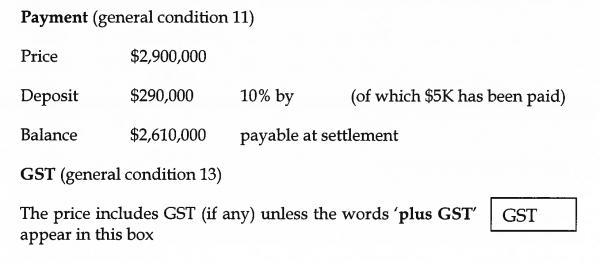

In November 2016, the Supreme Court of Victoria found that the sale of a Ringwood property for $2.9 million was inclusive of GST, as the particulars of sale included only the word “GST” in the box dealing with GST treatment, rather than “Plus GST”. See below:

By failing to include the word “Plus” before “GST”, the Supreme Court held that the vendor was liable to remit $290,000 to the ATO from the sale price. That is an expensive mistake!

In December 2017, the Court of Appeal set aside the judge’s findings, and found that the purchaser was liable to pay the GST in addition to the purchase price of $2.9 million.

The Court of Appeal carefully applied the principles of contractual interpretation to determine what a reasonable businessperson would have understood by the letters “GST” in the context of the contract. In the appeal decision, it held that by inserting the letters “GST”, the parties had intended that the purchaser would be liable to pay the GST amount to the vendor in addition to the price.

While the Court of Appeal decision may be regarded as the common-sense outcome by many, the circumstances surrounding the dispute highlight several important lessons for property developers:

1. The importance of careful drafting

It is essential to ensure that the contract of sale correctly sets out whether the price includes or excludes GST. Further protections can be incorporated into the contract by way of special conditions. Had this occurred, the expense of litigation over a four letter word could have been avoided.

2. The importance of proper due diligence before purchasing a property

Any due diligence should carefully consider the allocation of liability for GST under the contract. This is especially important if the land has commercial potential as a development site, as was the case here.

The Ringwood property was sold with a planning permit for construction of 10 dwellings. The purchaser had argued that as the property included an existing dwelling, GST was not payable.

However, the vendor had formed that view that as the property was not fit for habitation, it did not fall within the legal definition of residential premises, and GST was payable on the supply.

In such circumstances proper due diligence would assist in identifying the discrepancies, allowing the parties to attempt to resolve the issue before entering into a binding agreement.

3. The importance of expert advice on GST treatment

As illustrated, even property developers and their advisors can form differing views as to the correct GST treatment of the sale of land. Experienced, expert legal advice can assist in correctly identifying GST treatment and appropriately allocating liability for GST.

Please contact Mark McKinley, Principal on (03) 8640 2357 or Morgan Scholz, Senior Associate on (03) 8602 7244 if you would like any further information.

If you'd like to stay up to date with Russell Kennedy's insights, please sign up here.